Sycamore Portfolio Update | Q1 2026

Updates on each stock in the portfolio and Q1 performance, current holdings, etc.

Q1’s Contributors and Detractors

Let’s just say Q1 was marked by two primary detractors, with minimal contributors.

The two primary detractors in both percentage terms and absolute dollar amounts were PayPal and The Trade Desk. This shouldn’t come as a surprise if you’ve been following along.

I wrote about PayPal in early February and my decision to take a loss and move on, so no need to revisit that here. But TTD has been a different beast. The stock is down a shocking 40%+ YTD. Yes, I’m shocked by this.

I’ve written about it extensively, but the bottom line is that the company is working through a meaningful structural transition, shifting from a model more reliant on internal agency relationships toward one built on direct integration with brands and publishers, all while navigating sentiment headwinds tied to AI disruption. The company has continued innovating, which is partly the problem. They haven’t helped themselves through the Publicis situation.

On Publicis, if the company really is obfuscating fees for clients, they need to acknowledge it and fix the problem immediately. Management says they did not. If there’s a problem, fix it. Unacceptable if true.

But beyond this, something bigger and more structural seems to be at play. TTD continues to innovate, somewhat ironically given the previous paragraph, on transparency, objectivity, and supply chain efficiency. By nature of what they’ve built with OpenPath and the traction it’s seen over the last year or so, it makes a lot of sense that the large holdcos (Publicis, Omnicom, etc.) would have a vested interest in seeing TTD fail.

Their business models are built on principal media buying, where the holding company purchases ad inventory with its own capital upfront, takes on the financial risk by buying in bulk at a discount, and then resells that inventory to clients at a markup. The agency and the brands they represent are on opposite sides of the transaction. Not a business I would want to be in.

So it’s not the least bit ironic that these same players are hammering TTD on transparency and fees when opacity is literally their profit center.

Make no mistake, these audits are about OpenPath.

As I said, if TTD did screw up the Publicis relationship, my guess is it’s a one-off. Structurally, TTD is built on transparency and has historically been the most transparent actor in the adtech industry.

It’s worth noting that Omnicom launched an audit of their MSA (master service agreement) with TTD and found no issues. Even so, because it’s the name of the game right now, they hired a Big Four accounting firm to forensically review the entire relationship and dig up anything they can. That’s still a pending development.

The bottom line is TTD wins when the brands running through their platform win. That structural alignment means TTD, while down, is most certainly not out. In the long-term, the advantage goes to the company with the most objectivity and alignment with its customers. I believe that, and I’m sticking with TTD.

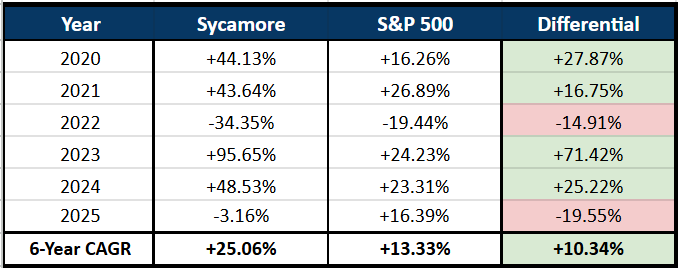

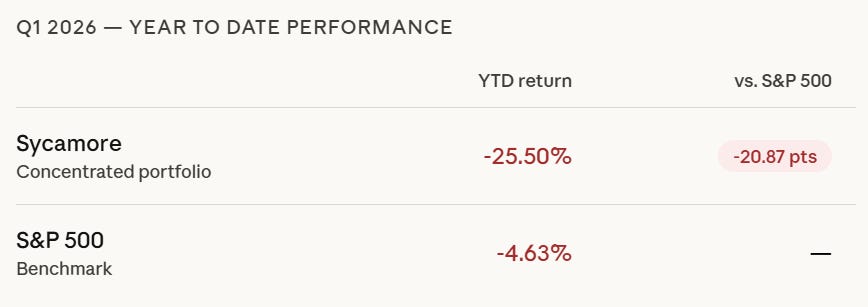

Q1 Performance

I’m not proud of the painful Q1, but I’m also not afraid of it either. Anyone writing a newsletter who only shows you their wins and never a loss or a drawdown, is not a real investor, nor honest.

Better days are ahead and beyond TTD, I like how the remainder of my portfolio is situated right now.

The long-term arc of Sycamore is still very much intact.