S&P Global (SPGI) | The Necessary Backbone of Global Capital Markets

One of the most strategically advantaged companies in the world and in a 25% drawdown.

S&P Global is one of the most strategically advantaged companies in the world.

It operates as the essential infrastructure layer of global capital markets, providing the credit ratings, benchmarks, data, and analytics that financial professionals, governments, and corporations rely on to make critical decisions every day.

With an over $15B revenue base, adjusted operating margins of ~50%, and over $5B in annual free cash flow, S&P Global is a compounding machine.

What makes S&P Global particularly compelling for the decade ahead is that its competitive position is strengthening. The company sits atop one of the deepest proprietary data reservoirs in financial services.

In an era where the winners of AI, in my opinion, will often be defined by the originators and owners of the highest-quality data, S&P Global’s position is very strong.

This analysis will look through S&P Global’s business model, its proprietary data moat, why it stands to be an AI winner, and the investment opportunity with the stock in a 25% drawdown.

The Business Model

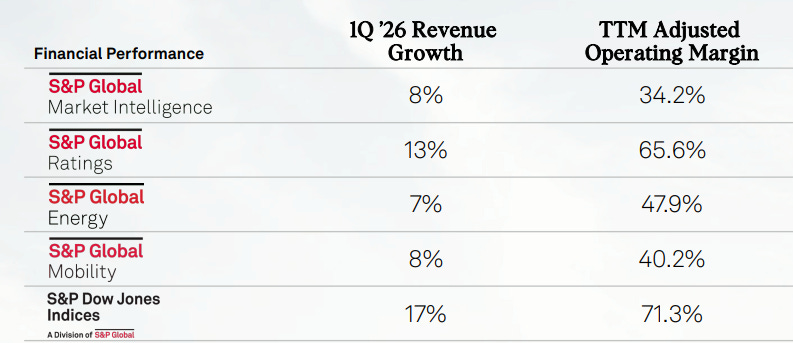

S&P Global operates through five divisions, each dominant in its market.

Ratings (~$4.4B revenue, ~66% operating margin) is the world’s largest credit rating agency. Issuers must obtain ratings to access capital markets. Investors are often mandated by regulation to reference them. This captive, repeat-purchase dynamic combined with near-zero marginal cost per opinion explains the 60% margin. The division grew 31% in 2024 as debt issuance volumes surged.

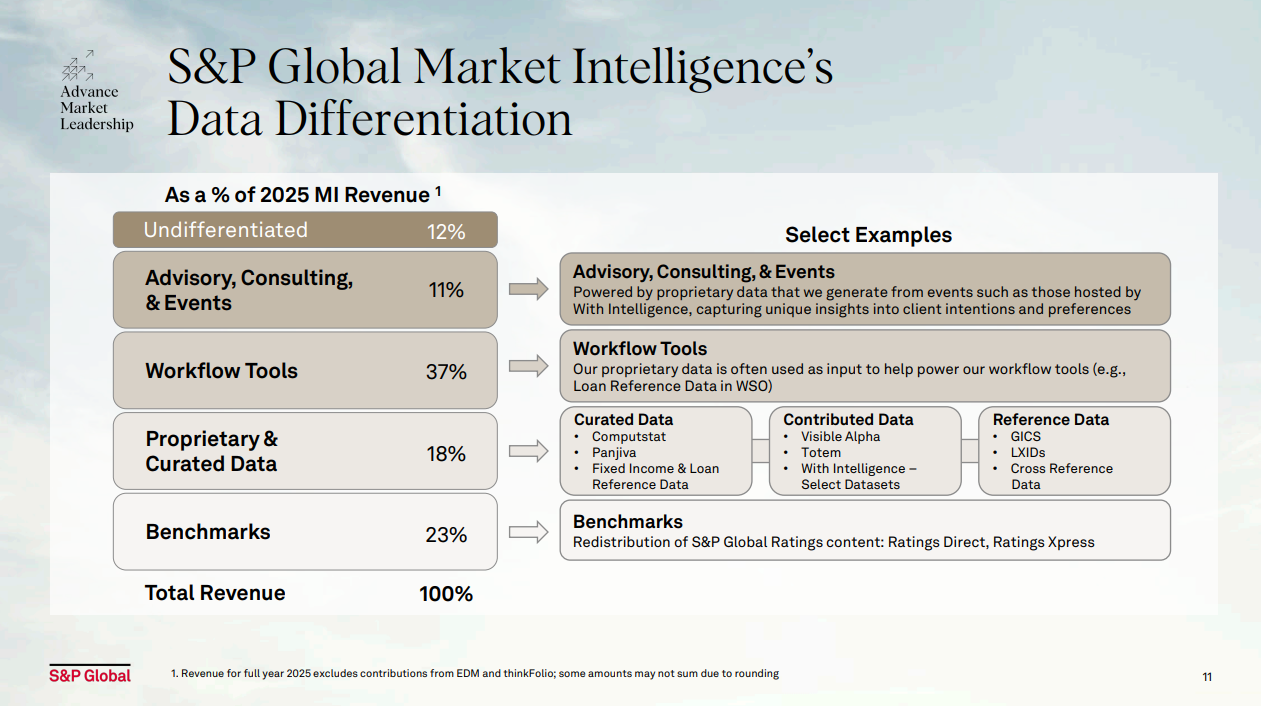

Market Intelligence (~$4.7B revenue, ~34% operating margin) is the data and analytics backbone, anchored by Capital IQ Pro. Subscription-based, high retention, and growing at 8% in Q1 2026, with margins expanding 160 bps Y/Y to 34.2%. The 2025 acquisition of With Intelligence expanded its private markets coverage. Early AI adoption signals are strong as customers who have purchased at least one AI product are growing annualized contract value at 1.3x the rate of other customers. More on this below.

S&P Dow Jones Indices (~$1.6B revenue, ~71% operating margin) stewards the S&P 500 and DJIA. It earns asset-linked fees from trillions in passive investment products benchmarked to its indices. The S&P 500 is the default benchmark because everyone else uses it. This self-reinforcing standard has no credible challengers. The global shift to passive investing is a permanent tailwind even if I personally dislike passive investing.

Commodity Insights (~$2.1B revenue, ~48% operating margin) is the dominant provider of benchmark prices for global energy, metals, and agricultural markets. Platts assessments are the reference price written into physical supply contracts worldwide. Once embedded in legal infrastructure, nearly impossible to displace.

Mobility (~$1.6B revenue, ~40% operating margin) includes CARFAX and automotive analytics. It is being spun off tax-free in mid-2026, allowing S&P Global to concentrate on its four core financial data businesses and enabling the market to separately value the higher-margin core.

Of these five business segments, the fastest growing as of Q1 2026 are Indices and Ratings. Both are growing double digits, and both carry the highest margins by a wide margin.

The Proprietary Data Moat

The moat is not built on a single dataset. It is the accumulation and integration of decades of structured, curated data across credit, finance, commodities, etc. that competitors cannot replicate.

Three layers define it.

Original intellectual property. S&P’s credit ratings, Platts benchmark prices, and index compositions are proprietary constructs originated through original methodology that serve as the foundation of global financial infrastructure. Said another way and importantly, this data is not an aggregation of public data.

Historical depth. Capital IQ tracks over 26M entities with decades of linked financial data. Commodity Insights holds 160+ years of commodity market history. Recreating this from scratch would take decades, cost billions, and is a functionally insurmountable barrier.

Regulatory and ecosystem embeddedness. In many cases, S&P data is legally required. Bank capital requirements reference credit ratings. Insurance regulators mandate them. Investment mandates are written around them. The S&P 500 is embedded in the legal structures of trillions in ETFs and index funds. Platts prices are written into physical commodity supply contracts worldwide. You cannot simply switch as the data is part of the architecture.

The 2022 merger with IHS Markit ($44B) was a defining expansion that paired S&P’s financial data strength with IHS’s energy, transportation, and supply chain intelligence.

Put all this together, and these layers work together and compound the moat around SPGI’s business.

Why SPGI Wins in AI

AI models are only as valuable as the data they are trained on. As stated, SPGI is the originator of some of the most valuable data in the world.

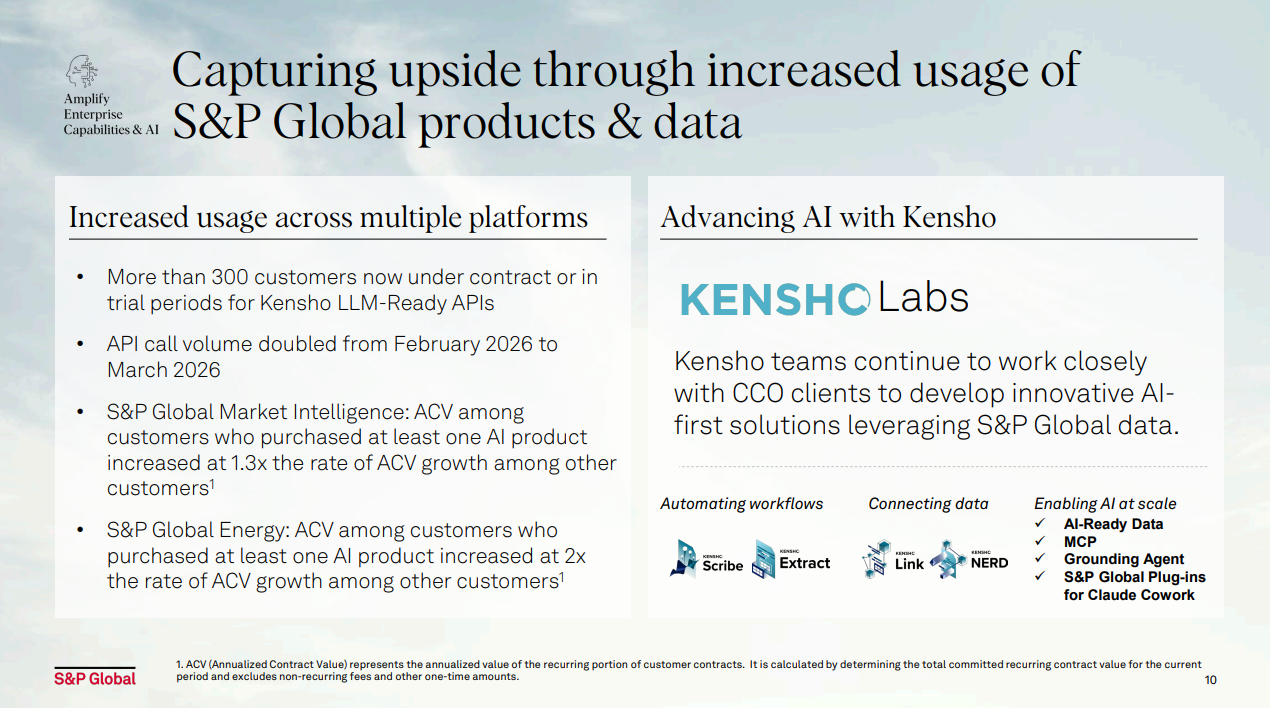

In 2018, ~5 years before generative AI became mainstream, S&P acquired Kensho Technologies for $550M. Kensho now serves as the company’s internal AI engine, developing models trained on SPGI’s domain-specific data. This is narrow and deep domain specificity that creates a real advantage in professional use cases.

Kensho’s core products: Scribe (financial audio transcription), Extract (structured data from complex PDF filings), NERD (named entity recognition linked to 26M+ entities), and Link (maps client data to S&P’s standardized identifiers). More recently, Kensho has expanded into AI-Ready Data, a Grounding Agent, MCP connectivity, and plug-ins for frontier AI platforms.

Over 300 customers are now under contract or in trial for the LLM-Ready APIs, with call volume doubling between February and March 2026 alone.

S&P has moved to make its data indispensable across every major AI platform rather than compete.