Inflection Points | Sycamore Portfolio Update [January 2025]

Monthly returns, current holdings, January transactions, selling Amex, and inflection points at NIKE

“So the whole idea of diversification, if you’re looking for excellence, is totally ridiculous.”

Charlie Munger, Berkshire Hathaway

Monthly Returns

Sycamore Capital Portfolio // +7.74%

S&P 500 // +2.70%

Differential // +5.04%

Year-to-date Returns

Sycamore Capital Portfolio // +7.74%

S&P 500 // +2.70%

Differential // +5.04%

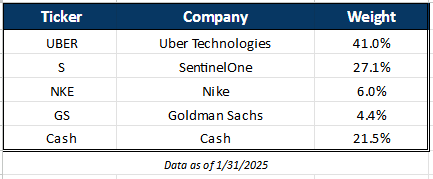

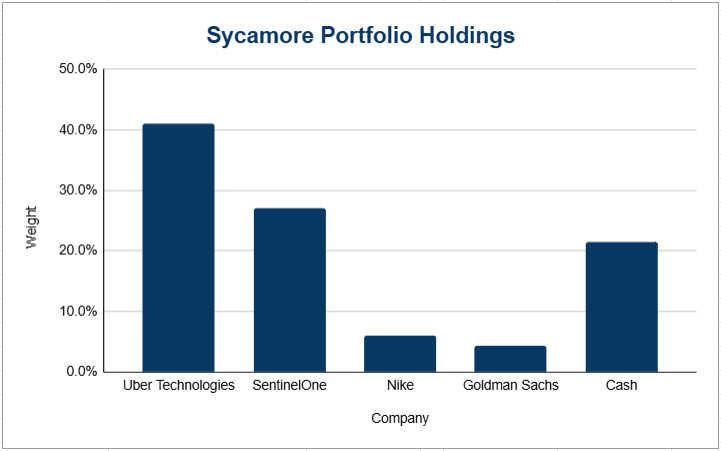

Current Holdings (as of January 31, 2025)

Transactions in January

Initiated NKE 0.00%↑ with 6.0% position at $71 /sh

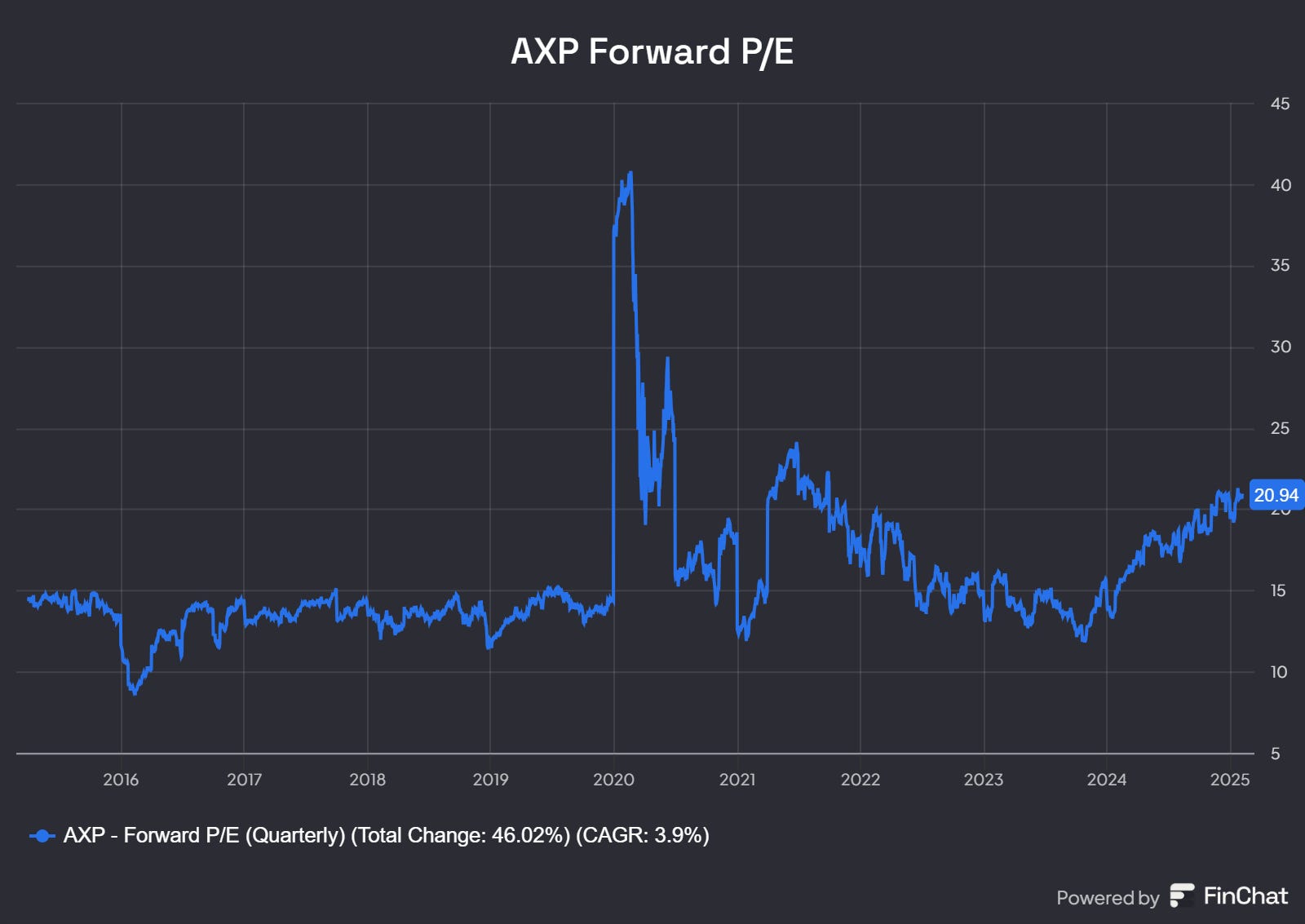

Sold out AXP 0.00%↑ at ~$310 /sh

American Express

I decided to go ahead and sell my American Express shares for two reasons:

Decelerating Revenue Growth: Amex grew revenue at 15% y/y in 2023 and 9% y/y in 2024. Still a very strong number on a $60B+ revenue base, but the company has aspirations for consistent 10%+ growth and they are already toeing the line on missing that target.

Elevated Valuation: Amex is a great business, and I’d have no problem holding the shares despite the deceleration in growth. Their momentum among Millennials and Gen Z remains strong (a point I’ve stated many times over the past 18 months), and the company is well-positioned for long-term growth. The issue is valuation as the stock is trading at an all-time high P/E multiple (ex-COVID). In my view, a lot of the gains have likely been pulled forward, with the stock up 60% in 2024. The multiple has expanded from 14x in 2022, when I initiated the position, to 21x today. I’d happily buy back in if it returned to more historical average levels.

NIKE: Inflection Points

Inflection Point: “(in business) a time of significant change in a situation; a turning point.”

In January, I took a position in Nike. My thesis is simple: Nike is at the crossroads of multiple inflection points in its business. While management works to right the ship, the brand remains one of the most recognizable and respected in the world, with deep, long-term partnerships across professional sports leagues, teams, and players.

I don’t know where the bottom is on this stock, but it’s trading near a five-year low. That said, the swoosh is everywhere, more than I even realized before paying closer attention. Nike also has a strong balance sheet, giving it the flexibility to navigate these inflection points while continuing to buy back shares and grow its dividend.

With that in mind, here are a few key inflection points I believe Nike is working through. If successful, this could be a high-quality investment in 2025.

Elliott Hill

Elliott Hill has an incredible career story. He left a job as a trainer with the Dallas Cowboys to start as an intern at Nike in 1988, rising through the ranks to retire as President of Consumer & Marketplace. When asked by a stranger on the street what he did for work, he humbly says he “sold sneakers and t-shirts for a living (source).” Now, he’s back out of retirement as CEO.

This guy is a winner, and I don’t think the world knows it yet. No one understands the Nike brand and business better than Hill, as the interview below reveals in great detail.

In my research, I found only the one full-length interview with Hill from a small, under-the-radar podcast in Fort Worth, TX with just 6K views.

The biggest takeaway? Hill knows his priorities.

When asked about his greatest career achievement, he didn’t mention being the driving force behind taking the Jordan brand global or Michael Johnson’s gold shoes at the ’96 Olympics in Atlanta (video), though he was. Instead, he honored his wife for the sacrifices she made for their family, saying his greatest achievement is that after 30+ years of marriage and a demanding career, they’re still best friends. The question that has weighed on him the most throughout his career: Did I do the right thing for my family?

Sycamore places family above all else, and hearing that kind of reflection from the CEO of a $100B+ business is rare. Regardless of what you think of Nike, you want Hill to succeed. I like aligning my bets with those kinds of people.

For Nike, Hill’s leadership is the defining inflection point, one that sets the stage for everything else I discuss below.

Prioritizing Wholesale Partners & Re-orienting DTC

One of the key reasons for Nike’s underperformance has been its aggressive focus on direct-to-consumer (DTC), its own website and app, at the expense of long-standing wholesale partners. This strategy has caused several issues:

Nike prioritized its best products for DTC, limiting availability in retail stores and allowing competitors like On and HOKA to gain prime shelf space.

By keeping its top-tier products online, Nike inadvertently hurt its own brand perception. The lower-quality inventory stocked in stores made it seem like the brand was in decline.

The shift strained long-standing wholesale relationships, causing unforeseen damage to a critical distribution channel.

Hill has made it clear that this was a major misstep and that repairing these partnerships will be a priority going forward. His focus on this area is especially important given his background, which includes decades of direct experience working with Nike’s wholesale partners. He understands the strength of these relationships and the role they play in Nike’s long-term success.

That said, while Nike’s DTC strategy has had flaws, the platform itself is a competitive advantage. The website and app are excellent. The issue has been how the company has used them, keeping the best products exclusive to DTC and leaning too heavily on promotions. If the new leadership team can fix this approach, the channel has real power.

In 2020, Nike processed 5 million DTC shipments. By 2024, that number had surged to over 70 million annually, equivalent to 133 shipments every minute. That level of technological capability is a huge asset. The key will be integrating DTC effectively without undermining wholesale.

Elliott will put things in order.

Other Inflection Points

Prioritizing Innovation

Nike has fallen behind in innovation and experimentation. Hill sees this as a major issue and is determined to change it. His plan is to clear the deck and aggressively introduce fresh, cutting-edge products into the marketplace. Expect a renewed focus on pushing boundaries and re-establishing Nike as the leader in performance-driven innovation in 2025.

Clearing Inventory

To make room for this wave of new products, Hill is focused on clearing out excess inventory. Short-term pressure is likely, but how aggressive Nike gets with promotions and how much this impacts margins will be something to watch.

Refocusing the Brand on Sport

Nike became great by being synonymous with greatness in sport. For decades, its products and storytelling were built around elite performance. Hill believes the company has lost that focus, and he intends to bring it back quickly. His experience working with Nike’s greatest athletes like Michael Jordan, Bo Jackson, and LeBron James gives him the edge and the expertise to ignite this part of the business in a way no one else can.

In 2025, we should expect to see more aggressive partnerships with players, teams, conferences, and leagues. Just as important, Nike will likely reorient its ad campaigns around the core narrative that built the brand: the relentless pursuit of excellence in sport.

Risks

Margin Pressure from Inventory & Wholesale Rebuild

Clearing excess inventory and rebuilding wholesale relationships could weigh on profitability. Heavy discounting may compress margins, while offering better terms to retailers could impact revenue mix. If Nike mismanages this transition, margin erosion could persist longer than expected.

Execution Risk in Innovation

Nike is pushing for a major product refresh, but success isn’t guaranteed. Competitors like On and HOKA have gained traction, and Nike must deliver compelling innovations to regain lost ground. Delays or underwhelming releases could further weaken its position in performance footwear.

Brand Repositioning Challenges

Shifting back to a sport-first identity is necessary but risky. Nike has leaned into lifestyle and fashion in recent years, and a sharp pivot could alienate certain consumers. If the messaging doesn’t resonate, the brand risks losing momentum with key demographics.

Bottom Line

Nike has several major inflection points converging in 2025, but in my view, they all hinge on Elliott Hill. So, I’m betting on an indelible brand and its new leader to get things back on track. I want Hill to win, and I want to win when he wins.

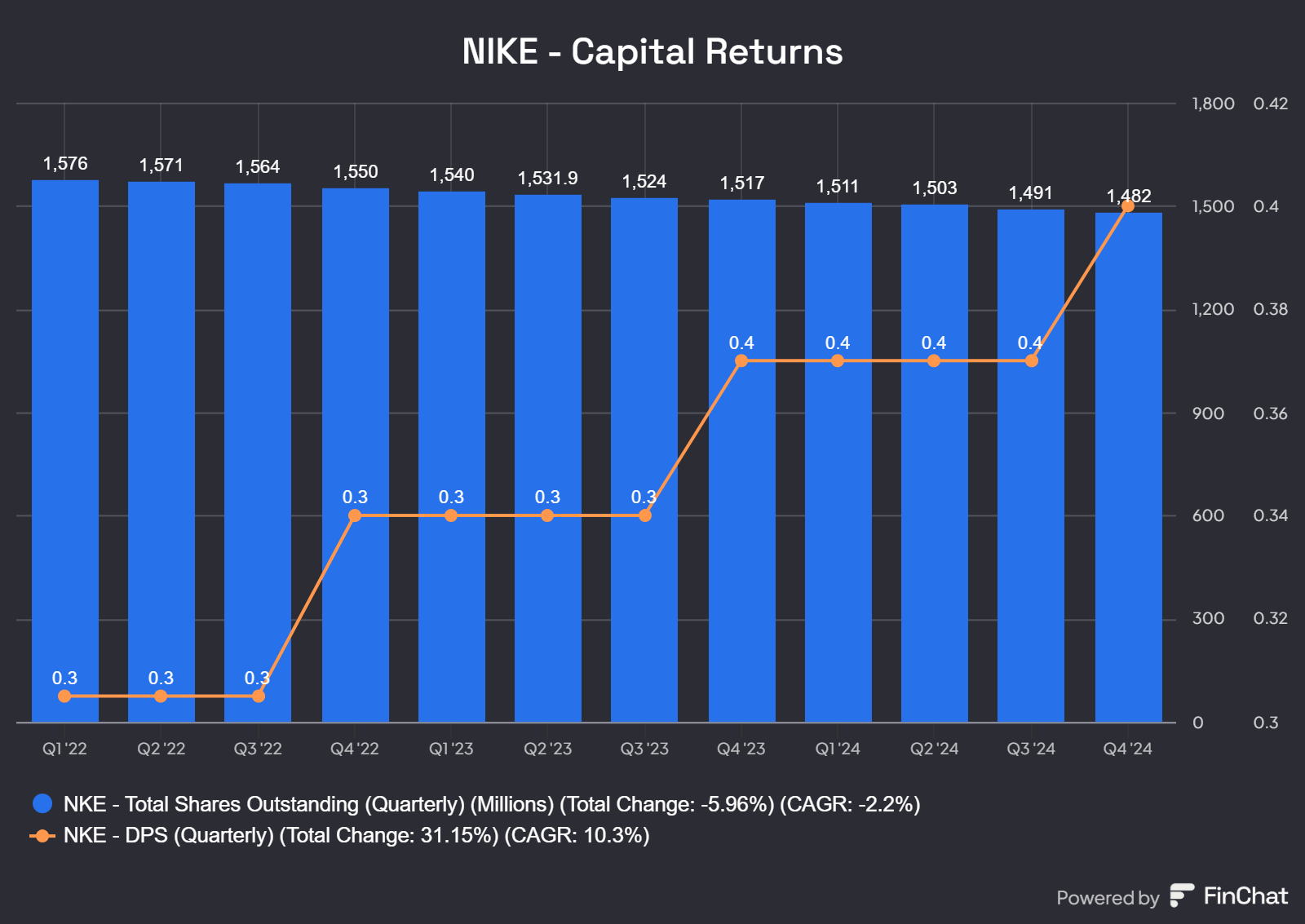

And while the stock works through these inflection points, I think we will continue to see capital returned to shareholders with 2% annualized reduction in shares outstanding and 10% annualized dividend growth.

You have definitely called it with Uber, and I applaud your analysis of Nike…all we can ever do is follow a plausible thesis and react to future events as they occur. Just do it!

I agree with your positions in Uber and SentinelOne, as well as your decision to exit American Express. I don't know enough about Goldman Sachs to have a view. I also respect and salute your willingness to put it all out there.

However, Nike seems a mistake. Even at $70 they'll have a hard time sustaining the earnings required for their over-stretched PE. Shifting from direct to retail further presses their margins, meaning sales need to grow that much more just to keep earnings flat. Nike needs significant earnings growth just to sustain its current valuation.

I don't think a turn around is likely. It is even less likely if the new CEO keeps talking about consumer weakness. Nike is full of Boeing and Intel levels of internal management speak excuses and the new CEO is not calling it. Nike is being hammered by 'consumer weakness' in China while Lululemon with the same consumers was up over 20% last quarter in China. Plus, being an obviously American consumer brand these days isn't going to help Nike in non-US markets. China, for instance.

I see Nike as more of stock in transition to being valued like General Motors. Still has a fabulous brand (Cadillac) but needs a PE under 10 to sustain the dividends and buy-backs.