A Premium Asset | Sycamore Portfolio Update [April 2025]

Quote, monthly & YTD returns, current holdings, April transactions, first thoughts, Uber AV update, Trade Desk thesis, and upcoming posts

“The whole secret of investment is to find places where it’s safe and wise to non-diversify.”

Charlie Munger

Monthly Returns

Sycamore // +4.48%

S&P 500 // -0.76%

Differential // +5.24%

Year-to-date Returns

Sycamore // +5.57%

S&P 500 // -5.31%

Differential // +10.88%

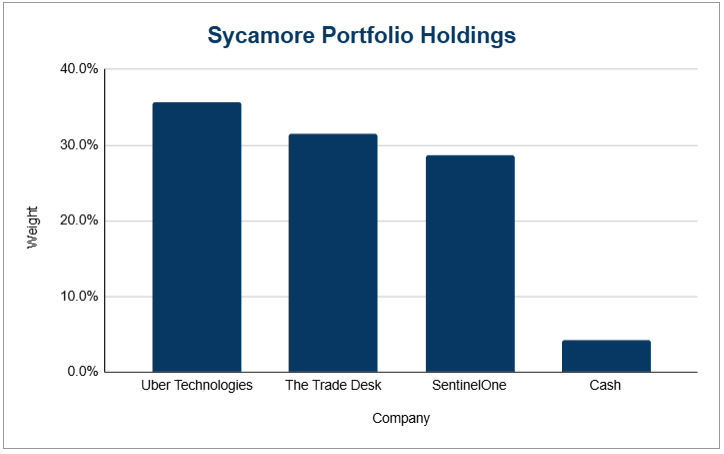

Current Holdings (as of April 30, 2025)

Transactions in April

Increased TTD 0.00%↑ by 32.8% at ~$48 /sh

Increased S 0.00%↑ by 6.4% at $16.50 /sh

Decreased UBER 0.00%↑ by 22.9% at ~$75 /sh

First Thoughts

I decided to trim my significant overweight position in Uber amidst the volatility throughout April. It is still my largest and highest conviction name in the portfolio.

I had originally targeted a 30% weighting in the portfolio. I moved aggressively to 40% when the stock dropped into the high $50s during the AV sell-off in Q4 2024. It was never meant to be a long-term allocation. It was a move to capitalize on short-term depressed sentiment and price action. That has worked well, with Uber outperforming the S&P 500 by about 40% YTD through April. With that result, I felt it was the right time to trim it back closer to my original target weight (which I’m still not there yet!).

I also used most of the proceeds to purchase additional shares of The Trade Desk and SentinelOne during a period of severely depressed sentiment in both stocks.

Uber AV Update

Uber’s AV team continues to fire on all cylinders. Over the past eight days, the following partnership announcements were made:

Volkswagen: a multi-year partnership to deploy thousands of autonomous, all-electric ID. Buzz vehicles starting in Los Angeles in 2026 (source).

May Mobility: a multi-year partnership to deploy autonomous, hybrid-electric Toyota Sienna vehicles on the Uber platform, starting in Arlington, Texas by the end of 2025 (source).

Momenta: a strategic partnership to launch autonomous robotaxi services in international markets, beginning in Europe in 2026, leveraging Momenta’s proven AV platform already deployed across multiple Chinese cities (source).

The thesis on Uber and autonomous vehicles is simple: a fragmented AV market plays directly into Uber’s hand. If Tesla ends up owning 90%+ of the robotaxi market, as Elon has promised, Uber’s ride-hailing business is effectively a zero. But if the industry remains competitive and fragmented, which I believe it will, Uber becomes the ultimate AV winner by serving as the demand aggregator that provides AV companies with the highest possible fleet utilization.

So far, what Elon promises is one thing, but what we actually see happening on the ground with Waymo, WeRide, May Mobility, Momenta, Volkswagen, Motional, Wayve, and others is something else entirely. My large, concentrated, and high-conviction bet is that the AV market will end up being highly fragmented across providers and geographies, and Uber will be the name that brings it all together.

If this thesis holds, Uber is a great asset to own at 21x FCF.

A Premium Asset in The Trade Desk

The Trade Desk is not a stock that’s new to me.

I first bought it in the fall of 2016, not long after the IPO. At the time, it was the largest investment I had ever made, and I held it all the way from a $2.50 cost basis (split-adjusted) to $75/share, exiting in late 2020. A 30-bagger in four years.

Since then, I kept up with the business, but had remained on the sidelines until last month.

Between mid-February and early April, The Trade Desk got hit with a perfect storm of problems, sending the stock down nearly 70% peak to trough. A brutal drawdown.

The company missed guidance for the first time in its history as a public company, ending a streak of 32 consecutive quarters of beats (incredibly impressive).

The stock had been priced for perfection (beyond perfection?) with no room for error.

And just as the miss drove the stock from the $120’s to the $60’s, we got a full-blown sentiment reset across growth and risk assets, accelerated by macro uncertainty and the tariff headlines. This drove the stock to its recent low of around $45 /share.

Put all that together and you had a premium asset trading like a broken company. That’s my kind of setup for a concentrated bet.

TTD Thesis

Jeff Green

Jeff is a true visionary and pioneer in the ad-tech industry. He has time and again predicted the future on where the industry and market is going. For example, he predicted Netflix would launch an ad-supported tier years before it happened. In a 2022 earnings call, he said:

“I think it's inevitable that every major streaming platform will have an ad-funded option. Consumers want choice, and the economics are too compelling to ignore.”

He’s been relentless about pushing the industry toward a more open, data-driven, and privacy-conscious future, and he has built the most important independent platform in programmatic advertising. That kind of leadership is hard to price in, but it's one of the core reasons I believe in this story.

Technology Leader and Innovator

The Trade Desk isn’t just maintaining its lead but is actively building the infrastructure for the future of digital advertising. OpenPath gives advertisers a direct line to premium publishers, cutting out the middlemen and reducing inefficiencies in the supply chain. UID 2.0 is TTD’s answer to the death of the third-party cookie: a privacy-conscious identity framework that puts control back in the hands of users while enabling precise, consent-based targeting. It’s gaining adoption across the ecosystem.

Ventura is The Trade Desk’s new streaming TV operating system, developed in partnership with smart TV OEMs and streaming aggregators. It aims to fix the messy state of streaming today by offering a cleaner ad supply chain, fewer but more relevant ads, better content discovery, and a more intuitive viewer experience. Built with OpenPath and UID 2.0 under the hood, Ventura gives advertisers sharper targeting, publishers better yield, and consumers a less annoying ad experience. Jeff Green put it simply: if the future of TV is ad-supported, the OS has to be objective, and The Trade Desk is stepping in with the neutral infrastructure to make it happen. Deployment is expected in 2025 with strong early industry support.

An Enormous TAM and Expanding

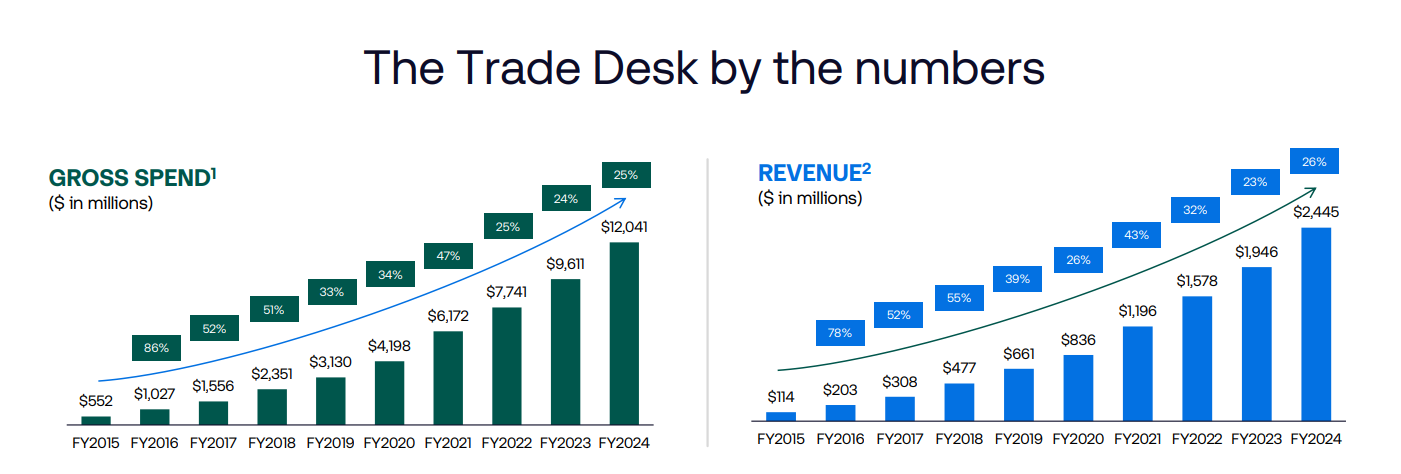

Global advertising spend surpassed $1 trillion in 2024, marking a significant milestone for the industry. The Trade Desk reported $12 billion in ad spend flowing through its platform in the same year, highlighting its growing influence in the digital advertising space. Connected TV (CTV) continues to be a major growth driver, with U.S. CTV ad spending reaching $30.1 billion in 2024, a 22.4% increase from the previous year. As streaming becomes the default, The Trade Desk is well-positioned to capitalize on this shift as a leading demand-side platform.

Elite Financial Profile

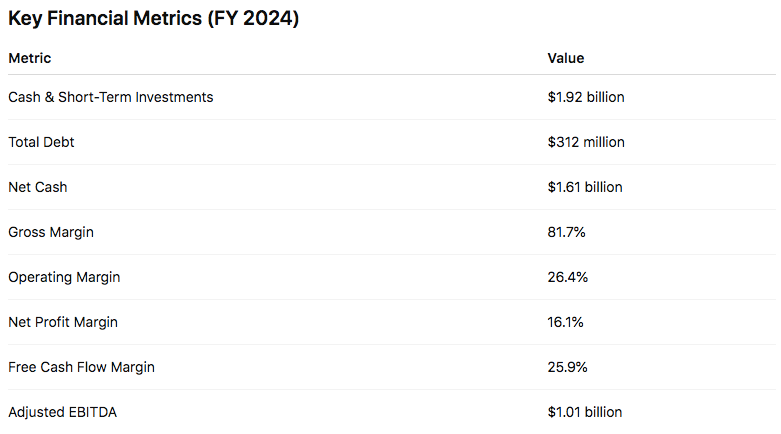

The Trade Desk continues to operate from a position of real financial strength. The balance sheet is rock solid with plenty of cash and minimal debt, giving the company flexibility to invest, weather volatility, or pursue strategic opportunities. Margins remain among the best in the industry with gross, operating, and free cash flow all reflecting how efficient and scalable the model is. The company has grown profitably from early on, showing discipline even as it scaled. They have now crossed the $1 billion mark in adjusted EBITDA, a major milestone. This is a durable business, growing quickly, highly profitable, and still founder led.

Upcoming Posts in May

We’re heading straight into Sycamore earnings season, and I plan to publish recaps following each portfolio company’s announcement:

Uber reports pre-market on Wednesday, May 7

The Trade Desk reports after the close on Thursday, May 8

SentinelOne reports after the close on or around Wednesday, May 28